ThinkGeoEnergy and Enerchange hosted Carlos Jorquera of PiensaGeotermia last July 1, 2022 on a webinar about the current status of geothermal development in South America. Carlos Jorquera is also President of the Geothermal Council, an organisation representing geothermal companies and developers in Chile.

The full recording of the webinar as shared below can be viewed via the official YouTube channel of Enerchange.

The contribution of Latin America & Caribbean to geothermal

From the first geothermal project in the region in Cerro Pabellon, the total installed geothermal capacity in the Latin America & Caribbean (LAC) region has now expanded to 1,716 MW. This accounts for about 10.8% of the total global capacity. Mexico contributes a majority of this capacity with 1,005 MW from five geothermal fields.

Recent developments in the region include the following:

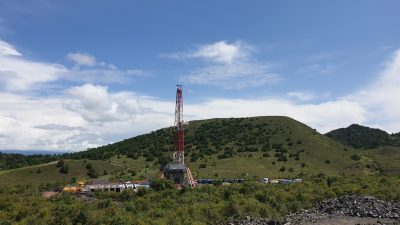

- In Chile, 33 MW of capacity was added to the Cerro Pabellon geothermal power plant in late 2021, increasing the total capacity to 81 MW;

- In Colombia, the first small-scale geothermal power plant with a 100-kW capacity was inaugurated in 2021. There are similar projects targeting geothermal production from existing oil wells with potential capacity of up to 700 kW.

- In Bolivia, the 5-MW Laguna Colorada pilot plant is close to completion. The long-term plan for the site is to use the pilot plant to power the construction of a 100-MW geothermal power plant.

Most of the existing geothermal projects in the LAC region are based on single-flash and double-flash power plant technology. However, the more recent developments have focused on binary technology. There is still huge potential for geothermal energy in the LAC region – more than 30 GW based on estimates.

The challenges of geothermal development in the region

The deregulated energy market has proven to be a disadvantage for geothermal in the LAC region as it is placed in direct competition with solar and wind. The analysis of the challenges was made under the context of Chile. For the past six years, the situation in Chile is similar to what is going on in Peru, Ecuador, Colombia, and Argentina.

In Chile, the energy strategy is driven by 2050 decarbonization goals. The aim of being carbon-neutral is also echoed by other countries in South America. Chile is one of the first countries in South America to create a strategy for exporting of green hydrogen and such efforts have also been replicated by Peru, Ecuador, and Argentina.

In 2015, Chile was one of the signatories in the Paris Agreement. This has led to the signing of an Energy Efficiency law that pushed the development of district heating and cooling systems with geothermal listed as a technology option. However, this law is still in its early stages as it was only approved last year.

There is currently no specific push to promote low-enthalpy geothermal use in South America. However, this is more prevalent in Central America where geothermal energy adds value to sectors such as agriculture. There is now also increasing preference for products with low or zero CO2 paths. This has affected the mining industry in Chile, Peru, and Argentina because of the copper and lithium typically needed by the electric vehicle industry.

Building new thermal plants is not possible in today’s market in Chile. Other countries, such as Peru and Ecuador, have more open markets for this technology as they are more reliant on oil and gas for power production.

Improving the energy auction in favor of geothermal

There are two types of energy auctions implemented in the LAC region. In Chile, the auction is driven purely by price. In Argentina, Peru, and Colombia, the auction is split into energy options per technology.

From Chile’s experience, an energy auction driven by price is not the right setup. It is unlikely for a geothermal power plant to be granted a PPA under this scheme because of the lower costs of solar and wind. As an example of solar and wind driving prices down, a solar plant got an offer for 18 USD/MWh last year.

To make geothermal competitive, there has to be value placed upon the flexibility and inertia provided by geothermal energy. Solar and wind can only provide synthetic inertia. The ability of geothermal to provide baseload capacity is something that solar and wind cannot emulate.

Smaller geothermal projects are unlikely to be developed in Chile because of the remote locations of potential resources. From a geothermal site, transmission lines between 60 to 100 kilometers need to be built. This forces the projects to be big – ideally 80 to 100 MW at the minimum.

To make geothermal projects more economically feasible, geothermal power is ideally sold to the grid and not to direct clients. Long-term PPAs are also sought-after, with a prescribed period of 20 to 25 years or more.

Geothermal energy as a premium energy source

Beyond being a source of power, geothermal is considered a premium energy source for overall economic growth. It adds value to sectors such as agriculture and food manufacturing through heating and direct use.

Lithium extraction from geothermal brine is also being explored in the LAC region. According to a preliminary analysis done by CEGA, extracting just 50% of the lithium content in the geothermal brine of the Cerro Pabellon site is equivalent to a PPA of 90 USD/MWh – practically equivant to having a new power plant.

Geothermal projects provide new and long-term jobs to surrounding communities. This has a cascading effect on the economies of the host regions. Moreover, the geothermal industry in Chile has healthy female representation and provides equal opportunities to different genders.

Source: Enerchange via YouTube